7 Ways To Save Big Money On Your 2020 Taxes—Part 2

2020 was a nightmarish year for many families. But thanks to recent legislation, you could see a silver lining in the form of major tax breaks when filing your income taxes this spring. First up, although it’s technically not a tax break, the IRS recently announced that the deadline for filing your 2020 federal income taxes has been pushed back from April 15 to May 17, 2021, which gives you an extra month to get your tax return handled.

The postponement applies to individual taxpayers, including those who pay self-employment taxes. But the extension does not apply to first-quarter 2021 estimated tax payments that many small business owners file. So if you file quarterly taxes, contact your tax advisor now, if you haven’t already done so.

Additionally, the CARES Act passed in March 2020 provides individual taxpayers with several hefty tax-saving opportunities, many of which are only available this year. What’s more, President Biden’s new relief package, known as the American Rescue Plan (ARP), which went into effect in March 2021, not only offers additional stimulus payments to most Americans, but it also includes significant tax relief for those taxpayers who lost their job and had to rely on unemployment benefits in 2020.

While there are dozens of potential tax breaks available for 2020, last week in part one of this series, we highlighted the first three of seven ways you can save big money on your 2020 tax return. Here in part two, we’ll discuss the remaining four ways you can save.

4. New Rules for Early Withdrawals From Retirement Accounts

If your finances were seriously impacted by last year’s economic turmoil, you may have needed to withdraw funds from your retirement accounts to cover your expenses. And thanks to new rules under the CARES Act, you have more flexibility to make an emergency withdrawal from tax-deferred retirement accounts in 2020, without incurring the normal penalties.

Typically, permanent withdrawals from traditional IRAs or 401(k) accounts are taxed at ordinary income rates in the year the funds were taken out. And pulling out money before age 59 1/2 would also typically cost you a 10% penalty.

But thanks to the CARES Act, you can avoid the 10% penalty (if under 59 1/2) on up to $100,000 in pandemic-related distributions from your retirement account in 2020. You are also allowed to spread such distributions over three years to reduce the tax impact. Or better yet, you can opt to put this money back into your retirement account—also within three years—and avoid paying taxes on the money all together.

However, because early withdrawals can negatively impact your retirement savings down the road, if you are looking to take advantage of this provision, you should consult with us, as your Personal Family Lawyer®, and your financial advisor first. Also, note that employers are not required to participate in this provision of the CARES Act, so you’ll also need to check with your plan administrator to see if it’s available at your workplace.

5. Medical Deductions

If you had hefty medical bills in 2020, you might be able to get some tax relief using increased deductions. Under the CARES Act, you can deduct any medical expenses above 7.5% of your adjusted gross income (AGI). Your AGI is your total income minus any other deductions you’ve already taken.

For example, if your AGI was $100,000, you can deduct qualified unreimbursed medical expenses that exceeded $7,500 in 2020. However, you have to itemize your deductions in order to write off these expenses, so meet with us to determine if this would make sense for your situation.

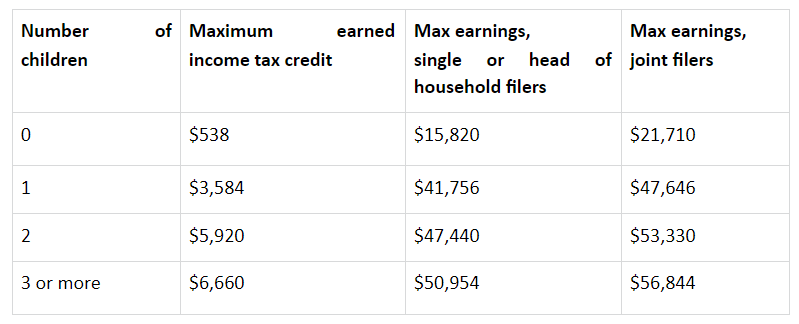

6. Earned Income Tax Credit

The Earned Income Tax Credit (EIC) is a refundable tax credit for low- and middle-income taxpayers that’s often overlooked. The amount of credit you can claim depends on your annual income and the number of kids you have—but people without kids can qualify, too.

Below are the maximum EIC amounts for 2020, along with the maximum income you can earn before losing the credit altogether. Note: You can't claim the EIC if you are a married individual filing separately.

Additionally, for the 2020 tax year, there are special rules for the EIC due to the pandemic: You can use either your 2019 income or your 2020 income to calculate your EIC and use whichever number gets you the bigger credit. This doesn’t happen automatically, though, so be sure to ask your tax professional to run the numbers both ways and choose the option that offers the most savings.

7. Child Tax Credit

If you have minor children aged 16 or younger, the Child Tax Credit is one of the most effective ways to reduce your federal income tax bill—and there are special rules for 2020 that can save you even more.

For your 2020 taxes, you can claim up to $2,000 per qualified child as a tax credit, and under rules due to the pandemic, you can use either your 2019 income or your 2020 income to calculate your credit—whichever year offers the most savings. The credit begins to phase out when your AGI reaches $75,000 for single filers, $150,000 for joint filers, and $112,500 for head of household filers.

What’s more, with the passage of Biden’s new ARP this March, the child tax credit is set to get even bigger in 2021. When you file your taxes next year, the per child credit will go up to $3,000 or $3,600, depending on your child’s age. Look for a future blog post detailing all of the new tax saving opportunities available under the ARP for 2021 and beyond.

Maximize Your Tax Savings for 2020

These are just a few of the numerous tax breaks available for 2020. Indeed, there are plenty of other deductions and credits that might be up for grabs depending on your situation. Meet with us, as your Personal Family Lawyer®, to make sure you don’t miss out on a single one. Contact us today to schedule your visit.

This article is a service of 20WestLegal LLC, Personal Family Lawyer®. We don’t just draft documents; we ensure you make informed and empowered decisions about life and death, for yourself and the people you love. That's why we offer a Family Wealth Planning Session™, during which you will get more financially organized than you’ve ever been before, and make all the best choices for the people you love. You can begin by calling our office today to schedule a Family Wealth Planning Session and mention this article to find out how to get this $750 session at no charge.